Transfer pricing (TP) has been considered a significant issue in tax audits in Vietnam in recent years. Many multinational enterprises with subsidiaries operating in Vietnam have fallen under the scrutiny of the Vietnamese tax authorities, indicated by the fact that TP-compliant documents have become one of the first pieces of information required in many tax audits.

In an effort to counter inappropriate TP conduct and create a better environment for doing business in Vietnam, the Vietnamese government has recently updated the national TP regime with the issuance of Decree No. 132/2020/ND-CP (Decree 132) on November 5 , 2020, effective from December 20, 2020 and applicable for 2020 assessment year onward in general.

With material revisions, amendments and supplements compared to the superseded Decrees No. 20/2017/ND-CP and No. 68/2020/ND-CP, Decree 132 has set out a new regulatory environment, bringing in many new advantages as well as challenges for Vietnamese taxpayers engaging in intra-group transactions.

The notable features of Decree 132 and associated implications for taxpayers will be discussed in this article.

First Come the Pros ...

Updated Definition of “Commercial Database”

The most significant advantage provided for under Decree 132 is the updated definition of “commercial database,” which is expected to ease up the research process and create a legal basis for taxpayers’ defense during tax audits.

Previously, an acceptable data source was merely limited to financials extracted from publicly available sources without any further guidance. This created significant inconvenience for taxpayers during their compliance work, due to the differences in both accounting standards and treatment as well as reporting language. For example, if taxpayers engaging in intra-group transactions, or their advisers in most cases, wished to examine whether their profit margin seemed compliant or not, they would have to go through thousands of financial statements and possible adjustments to figure out their position, without even taking into account the language barrier as well as non-comparable reporting, due to variance in accounting standards and treatment.

Decree 132 allows the use of commercial databases with retained, standardized and updated financial information. As a result, Vietnamese taxpayers will benefit from using standardized and uniform databases and might thus be unaffected by any non-comparable reporting, as well as being able to defend their research/study during tax audits.

Increase of Deductible Interest Expenses

Another significant advantage for Vietnamese taxpayers created by Decree 132 is the relaxed limitation of deductible interest expenses. Previous TP regulations provided that only 20% of earnings before interest, tax, depreciation and amortization (EBITDA) should be the maximum deductible interest expenses applied for taxpayers to claim within a tax assessment year, and any exceeding amount would go directly into tax trash. Such a limitation has been considered quite modest for taxpayers who enter into significant loans/borrowings, or particularly for new businesses with large usage of working capital, to the detriment of their tax planning and reporting.

Under Decree 132, the cap of interest expenses to be considered deductible for corporate income tax purposes has been lifted to 30% of the newly defined concept of net EBITDA, which provides a slight difference to take out financial income from savings and loans. It is of more importance that the amount in excess of this would not go directly to tax trash as required previously. Instead, such excess of the current assessment year will now be allowed to carry forward for a maximum period of five consecutive years, provided that taxpayers would not reach the provided cap in the future.

Obviously, taxpayers benefit not only from the expansion of deductible interest expenses but also from more flexibility in planning their utilizable deductibility in the upcoming period and managing their tax expenses in the long run.

But There Are Also the Cons ...

Narrowed Arm’s-length Range

Alongside the advantages provided for, Decree 132 also introduces some burdens for taxpayers in Vietnam, in our opinion. Possibly the most significant burden would be the narrowing of the acceptable arm’s-length range within which the pricing of intra-group transactions could be considered appropriate.

It is the TP concept of arm’s-length range that requires the taxpayer to set out and adjust their pricing mechanism or profit margin applied for controlled transactions to be similar to the uncontrolled or independent pricing range applied in comparable independent transactions. As per the Decree 132 regulations, taxpayers in Vietnam are required to aim their comparable price or margin higher than previously applied, since the minimum of acceptable arm’s-length range has been raised from the 25th percentile to the 35th percentile.

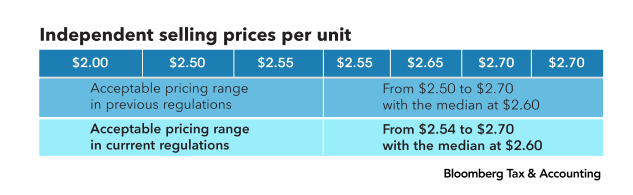

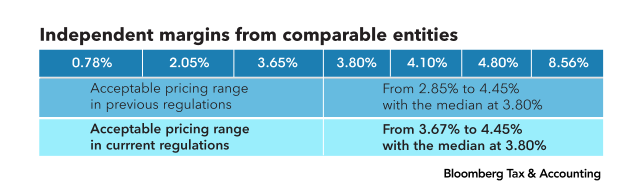

The following tables will provide a clearer explanation for ease of understanding.

For comparison of pricing:

For comparison of profit margin:

It is clear that taxpayers engaging in related party transaction(s) are now expected to result in a higher profit compared with previous reporting years, in order to be considered compliant and thus minimize the risks of being challenged by the authorities. This is also quite a distinctive requirement, if not an exclusive case in the world, adopted by the Vietnamese authorities. Vietnamese taxpayers should therefore now be very careful in planning and managing their tax position.

Expanded Definition of Related/Controlled Party

After years of adopting a typical definition of “related party” focusing on corporate relationships, the Vietnam government has now introduced an expanded definition of “related party,” covering also the individual–corporate relationship.

Accordingly, in cases where an enterprise incurred:

- capital transfer(s) totally equal to 25% of its owner’s equity or more; and/or

- lendings or borrowings totally equal to 10% of its owner’s equity, with its executive personnel or their immediate family;

such individual(s) should be qualified as a related party of that enterprise.

Obviously, such transaction(s) should be subject to compliance requirements of declaration and analysis to be included in the enterprise’s TP compliance documents. Businesses could be impacted by this expanded definition and are recommended to undertake proper planning and analysis to ensure their compliant positions.

Obligations to Submit Country-by-Country Report

Last but not least, a provision of Decree 132 on obligations of Vietnamese taxpayers to submit the country-by-country profitability report (CbCR) seems to require clarification.

In general, Decree 132 has provided the required information, template and deadlines for submission of the CbCR by an ultimate parent company in Vietnam. There is also a threshold for such taxpayers to be exempted from the CbCR requirement. For taxpayers which are Vietnamese subsidiaries of either or both Vietnamese and/or overseas ultimate parent companies, Decree 132 simply requires the observation of international tax treaties or agreements on automatic information exchange regime.

These provisions seem to be rather forward-looking, and thus further clarification from the relevant authorities might be required, as we are aware of neither international tax treaties nor agreements on automatic information exchange entered into by the government.

Conclusion

In brief, we have seen the government’s efforts in creating a legal counter to inappropriate transfer pricing actions but also ensuring the most friendly and equal business environment possible in Vietnam. With Decree 132, taxpayers can be more flexible in their working capital utilization and compliance arrangements.

However, the narrowing of the acceptable arm’s-length range and expanded definition of related party would likely create more burdens for companies in managing their tax positions.

At the same time, the requirements for CbCR exemption may require more effort not only by taxpayers but also by the authorities if a smooth implementation is to be aimed for.

In light of the above, taxpayers are recommended to conduct proper planning and consult with their advisers to be proactively compliant and have a strong defense in case of tax audits and/or inspection.

Source: https://news.bloombergtax.com/daily-tax-report-international/transfer-pricing-in-vietnam-new-regulatory-environment